By Marcos Vigil and Shari Blakey

Federal agencies must continuously adapt to evolving financial accounting standards and requirements. Implementing new financial and system processes is challenging, but critical to the successful adoption of new accounting procedures that can withstand financial audit scrutiny and prevent any negative or adverse impact on a federal agency’s long-standing unmodified (clean) audit opinion.

Effective October 1, 2023, the Federal Accounting Standards Advisory Board (FASAB) redefined lease reporting requirements through the issuance of Statement of Federal Financial Accounting Standards (SFFAS) No. 54, Leases, as amended.1 Federal agencies proceeded to take on the formidable task of being audit-ready by demonstrating to auditors that all relevant documentation is maintained (e.g., policies and procedures, lease inventory records), new or updated internal controls are operating effectively, and leases are appropriately recorded and/or disclosed in the financial statements.

SFFAS No. 54 Lease Requirements – What’s New?

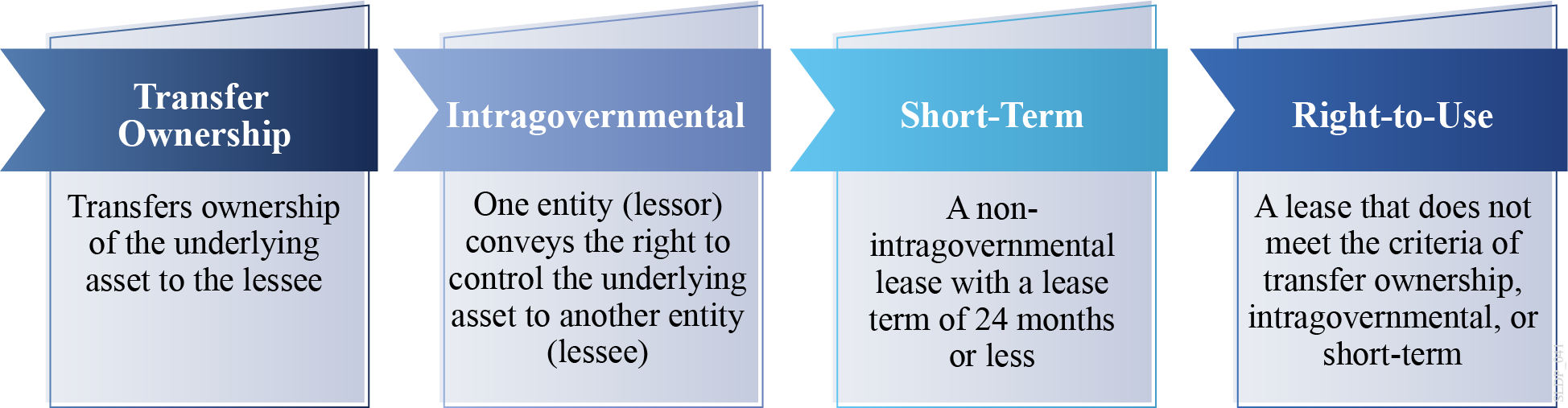

The traditional operating and capital lease categories used by all Federal agencies were replaced by four “new” lease categories: 1) contracts or agreements that transfer ownership; 2) intragovernmental; 3) short-term; and 4) leases other than contracts/agreements that transfer ownership, intragovernmental, and short-term (commonly referred to as “right-to-use” leases).

Note: Some general SFFAS 54 exclusions include leased assets under construction, leased internal use software (i.e., licenses). Refer to SSFAS 54 and FASAB Technical Release 20 for more details.

The fourth lease category, right-to-use leases, is now a broader category to identify, quantify, and disclose/report for financial accounting purposes (i.e., more than just a non-intragovernmental lease that expands beyond 24 months). Economic benefits realized from lease payments may qualify for the right-to-use asset lease category (i.e., benefits realized by the lessee for the use of the asset, benefits realized by the lessor for receiving lease payments). As a result, most lease arrangements (i.e., lease contracts/agreements and transactions) may fall under this category, elevating the risk in achieving completeness and accuracy for inventory and reporting purposes.

SFFAS No. 62 Embedded Leases – The Fifth Lease Category

In addition to the four lease categories, SFFAS 54 also requires Federal agencies to continually review all contracts and agreements to identify “embedded leases.” There are instances where complex contracts or agreements may contain both a lease and non-lease component. Generally, the lease component(s) and non-lease component(s) should be accounted for as separate contracts or agreements. However, due to challenges experienced in assessing these contracts/agreements, FASAB introduced SFFAS No. 62, Transitional Amendment to SFFAS 54,2 in November 2023 to allow for up to a three-year transitional implementation period for reporting “embedded leases.” SFFAS 62’s transitional accommodation applies only to contracts or agreements that meet both of the following criteria:

- The contracts or agreements contain non-lease component(s) and may contain lease component(s); and

- The purpose of the contracts or agreements is primarily attributable to the non-lease component(s), such as service components, based on management’s assessment of the nature of the contracts or agreements and professional judgment.

During this transitional accommodation period of October 1, 2023, to October 1, 2026, Federal agencies may elect to record “embedded leases” as a non-lease and account for the entire multi-component contract or agreement as non-lease. Therefore, Federal agencies must continue to prepare for lease guidance changes (i.e., “embedded lease” accommodation period expiration) and monitor any supplemental FASAB and other regulatory authoritative source requirements.

SFFAS 54 and 62 Compliance – Adhering to Audit Requirements (Standardization & Sustainment)

FY 2024 marked the first year of SFFAS 54 and 62 implementation, yielding promising audit results during the review of Federal Agencies’ FY 2024 audit reports. FASAB monitored implementation of the standards through the review of 32 consolidated entities, which noted seven consolidated entities with reportable audit findings in internal control associated with leases and SFFAS 54 adoption (three agencies obtaining material weaknesses and four agencies obtaining significant deficiencies), while 19 of the 32 consolidated entities elected to apply the SFFAS 62 transitional accommodation period.3

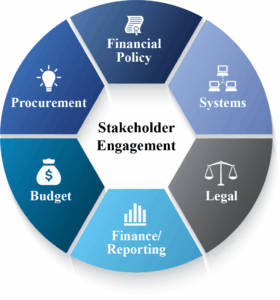

As a result, Federal agencies acknowledge further improvements are necessary to enhance its right-to-use and embedded lease internal control activities and efforts. Federal agencies shift their focus on responding to prior year audit findings and upcoming annual audit requests by focusing on post-lease implementation activities (application of lease day-to-day processes), evaluating current and new agreements to standardize right-to-use and embedded lease language (i.e., identify key indicators for right-to-use and embedded lease qualification), and re-evaluating materiality (i.e., annually) to identify key changes in its right-to-use and embedded lease activity. Federal agencies can accomplish enhancing its right-to-use and embedded leases business processes by focusing on three key components: 1) Stakeholder Engagement; 2) Lease Inventory – Completeness and Accuracy; and 3) Internal Control Enhancement – Design/Operating Effectiveness.

Stakeholder Engagement

Federal agencies should continue to engage with key stakeholders to obtain adequate representation and information from all respective program offices/departments (e.g., financial, operations/logistics, budget, procurement, systems). After a successful implementation of the lease standard, the focus of stakeholder engagement needs to shift to incorporate the initial right-to-use and embedded lease identification activities into the entity’s day-to-day application and operations to standardize lease policy, reporting, and system requirements.

Federal agencies should continue to engage with key stakeholders to obtain adequate representation and information from all respective program offices/departments (e.g., financial, operations/logistics, budget, procurement, systems). After a successful implementation of the lease standard, the focus of stakeholder engagement needs to shift to incorporate the initial right-to-use and embedded lease identification activities into the entity’s day-to-day application and operations to standardize lease policy, reporting, and system requirements.

Further, it enables Federal agencies to enhance and deploy cross-functional teams to collaborate on overlapping requirements, including, but not limited to:

- Finance and Accounting: Facilitate an update to the interpretation and application of the right-to-use and embedded lease standards through documentation into the Federal agency’s policies and procedures

- Operations and Logistics: Coordinate with Finance and Accounting to update lease inventory records and expand on right-to-use and embedded lease evaluation criteria to align with lease accounting and reporting terminology and requirements

- Legal and Procurement: Collaborate with Finance and Accounting to identify ‘indicators’ for right-to-use and embedded lease qualification to standardize contract and agreement language in a manner that facilitates and incorporates lease identification and classification activities into the normal procurement business processes

- Financial Systems: Identify and communicate unique system configuration and set-up. System updates require careful examination to minimize operational impacts and ensure compliance with new lease standards requirements (i.e., updating financial system posting logic to align with new United States Standard General Ledger [USSGL] requirements from the Bureau of the Fiscal Service).

Communication is critical for the effectiveness of stakeholder engagement across a federal agency’s programs and offices. Timely dissemination and clear communications to all stakeholders promotes compliance with the right-to-use and embedded lease standards.

Lease Inventory – Completeness and Accuracy

Federal agencies must continue to update their lease inventory listing, so it is complete and accurate in accordance with the new lease categories (i.e., right-to-use, embedded), terminology, and requirements. A key focus in updating a lease inventory listing will be the review of both current and new contracts and agreements to identify key indicators that qualify and meet the criteria of right-to-use and/or embedded leases that satisfy two key audit assertions:

- Completeness: Federal agencies will need to access and review all current and new contracts and agreements to assess whether these procurement arrangements qualify to be reported as right-to-use or embedded leases. Some factors that may prove beneficial in standardizing right-to-use and embedded lease inventories include:

- Develop and continuously monitor a listing of key points-of-contact that have accessibility for specific types of contracts and agreement documentation, especially if maintained in more than one physical/digital location (e.g., multiple non-financial systems). Given the time sensitivity of audit requests and limited federal resources, a centralized point-of-contact listing to reference improves efficiency and productivity in contract and agreement documentation retrieval

- Evaluate current and new contracts and agreements to identify, standardize, and document key procurement qualifying ‘indicators’ (i.e., factors, attributes) that meet the criteria of right-to-use or embedded leases. Subject matter experts such as procurement and legal personnel should be included in the evaluation of complex contract and agreement arrangements to analyze, identify, and standardize the determination criteria to be used going forward to categorize these complex contract vehicles into right-to-use or embedded leases. This will create efficiencies when evaluating new complex contracts and agreements since qualification and applicability criteria would be documented for future uses.

- Accuracy: Using the current leases inventory listing, Federal agencies will be required to continue to enhance its right-to-use and embedded lease inventories to identify additional information pertinent for required disclosure or reporting under SFFAS 54 requirements.

The compilation of a complete and accurate lease inventory listing is a critical aspect in substantiating to the auditors that a Federal agency continues to have appropriate procedures in place to identify its right-to-use and embedded lease records and disclose in its financial statements (as applicable) in accordance with the Office of Management and Budget (OMB) Circular A-136, Financial Reporting Requirements.4

Internal Control Enhancement – Design and Operating Effectiveness

After initial SFFAS 54 implementation (FY 2024 – Year 1), Federal agencies should reassess and identify necessary updates to their right-to-use and embedded lease internal control processes, which will differ from the internal controls and processes implemented during SFFAS 54 implementation. Federal agencies are required to document these updated internal controls and processes in accordance with OMB Circular A-123, Management’s Responsibility for Enterprise Risk Management and Internal Control,5 and the Government Accountability Office’s (GAO) Standards for Internal Control in the Federal Government (Green Book).6 The objective of the internal control enhancement is to incorporate the initial right-to-use and embedded leases business processes into the Federal agency’s normal day-to-day operations (i.e., sustainment), facilitating both the identification, evaluation and reporting of right-to-use and embedded lease arrangement in an efficient and timely manner. Potential internal control enhancement considerations include policies and procedures, risk assessments, accounting systems, and communication:

After initial SFFAS 54 implementation (FY 2024 – Year 1), Federal agencies should reassess and identify necessary updates to their right-to-use and embedded lease internal control processes, which will differ from the internal controls and processes implemented during SFFAS 54 implementation. Federal agencies are required to document these updated internal controls and processes in accordance with OMB Circular A-123, Management’s Responsibility for Enterprise Risk Management and Internal Control,5 and the Government Accountability Office’s (GAO) Standards for Internal Control in the Federal Government (Green Book).6 The objective of the internal control enhancement is to incorporate the initial right-to-use and embedded leases business processes into the Federal agency’s normal day-to-day operations (i.e., sustainment), facilitating both the identification, evaluation and reporting of right-to-use and embedded lease arrangement in an efficient and timely manner. Potential internal control enhancement considerations include policies and procedures, risk assessments, accounting systems, and communication:

- Policies and Procedures: Review and update existing lease-related policies and procedures to enhance compliance with right-to-use and embedded lease requirements

- Risk Assessment: Enhance internal control assessments over current right-to-use and embedded lease controls in place, identify any internal control gaps, and re-evaluate the design and operating effectiveness of updated internal controls in response to any prior year audit findings (i.e., post-implementation internal control sustainment – incorporation into day-to-day business processes)

- Accounting Systems: Update accounting systems and sub-ledgers, as necessary, to apply right-to-use and embedded lease accounting/reporting requirements (e.g., update posting logic based on new/updated USSGL and object classes)

- Communication: Formally communicate lease-related policy and process changes to agency personnel and conduct training to applicable staff to ensure an understanding of new processes.

Appropriate implementation of right-to-use and embedded lease-related internal controls and validating that these controls continue to be designed and operating effectively are essential in the continued success of upcoming annual financial statement audits.

What’s Next – Continuous Monitoring and Compliance

While SFFAS No. 54 and SFFAS No. 62 are fully effective, Federal agencies should perform continuous monitoring over their right-to-use and embedded lease internal controls to ensure they are operating effectively and as designed. Additionally, Federal agencies should continue to monitor evolving guidance as supplemental requirements may become available.

The next few years (i.e., FY 2025 – FY 2027) will consist of an internal control enhancement and sustainment period for Federal agencies as they adapt to the new lease requirements. Federal agencies should use this time to continue to update and mature right-to-use and embedded lease processes. Federal agencies and auditors will continue to collaborate to both identify areas where right-to-use and embedded lease procedures are operating effectively and prepare for the expiration of the SFFAS 62 transitional accommodation period, depending on the timeframe each Federal agency selected (one to three years).

Connect with Us

This publication is for informational purposes only and does not constitute professional advice or services, or an endorsement of any kind.

Kearney is a Certified Public Accounting (CPA) firm focused on providing accounting and consulting services to the Federal Government. For more information about Kearney, please visit us at www.kearneyco.com or contact us at (703) 931-5600.

1Statement of Federal Financial Accounting Standards 54: Leases https://files.fasab.gov/pdffiles/handbook_sffas_54.pdf

2Statement of Federal Financial Account Standards 62: Transitional Amendment to SFFAS 54 (Paragraphs 3-5). https://files.fasab.gov/pdffiles/handbook_sffas_62.pdf

3FASAB February 2025 Board Brief Materials – FY 2024 Leases Reporting and Audit Results (https://files.fasab.gov/pdffiles/25_02_Topic_C1_Leases_Combined_web.pdf)

4Office of Management and Budget Circular A-136: Financial Reporting Requirements (Part II.3.8.19 – Note 19 Leases) https://www.whitehouse.gov/wp-content/uploads/2023/05/A-136-for-FY-2023.pdf

5Office of Management and Budget Circular A-123: Management’s Responsibility for Enterprise Risk Management and Internal Control (Section IV. Assessing Internal Control, pages 29-32)

https://www.whitehouse.gov/wp-content/uploads/legacy_drupal_files/omb/memoranda/2016/m-16-17.pdf

6Government Accountability Office: Standards for Internal Control in the Federal Government (Control Activities – Principles 10 – 12, pages 45-56) https://www.gao.gov/assets/gao-14-704g.pdf