By Ryland Rumph

Artificial Intelligence (AI), Fraud Services, and Risks

AI is concept that has existed for decades; however, its application and significance has become prominent over the last decade. Accordingly, businesses and governments are adapting to its use. AI has opened new methods for fraud to be effectively committed within the financial and business worlds. Additionally, AI Technology and Data Mining can be used as a control to effectively monitor, prevent, detect and deter fraud and improper payment.

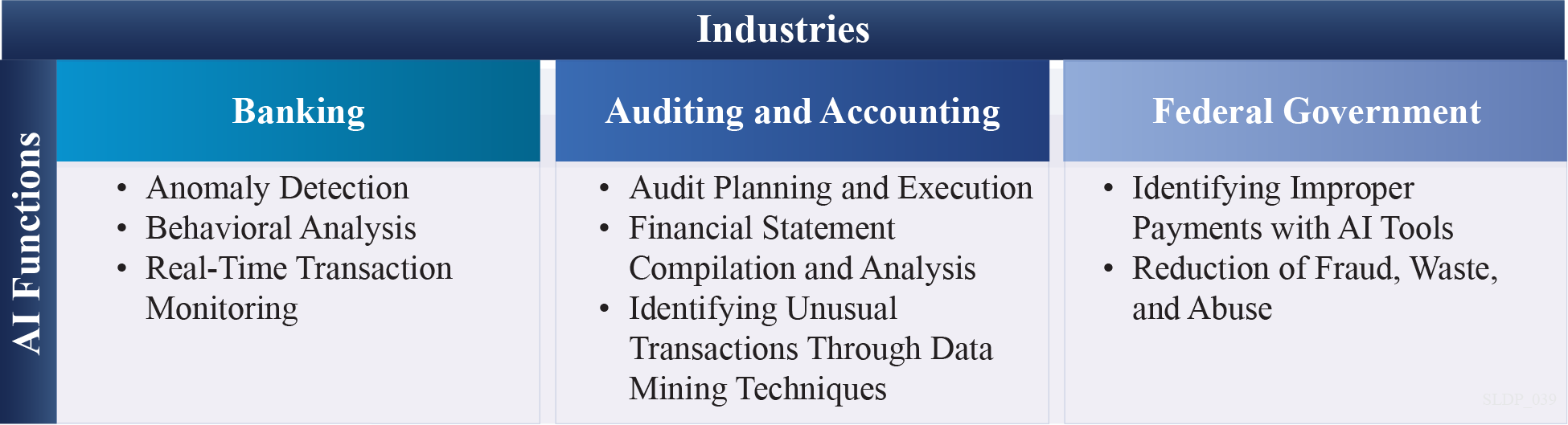

Figure 1: AI Functions by Industry

Business managers and auditors use AI to detect fraud. Audit and internal control standards, such as Auditing Standards required by the American Institute of Certified Public Accountants (AICPA) and Internal Audit and Internal Control programs required by law and regulations (i.e., the Government Accountability Office’s [GAO] Standards for Internal Control in the Federal Government [Green Book] and Federal Manager’s Financial Improvement Act of 1982 [FMFIA]), require inclusion of internal control services to detect, deter, and prevent fraud. These standards govern external and internal audits. Investigative services, which can be law enforcement mechanisms, or can be elective, include Fraud Examinations and Forensic Accounting. These industries and services are adapting to the AI environment and must become more sophisticated in understanding the impact and uses of AI to commit fraud, and in contrast, to detect, prevent, and correct fraud within the financial, accounting and regulatory professions. AI has created new means to commit fraud via e-mail phishing, voice mimicking, and the creation of fictitious transactions with false documents. For example, language learning models enable human-like writing of e-mails that are more relevant and are written without mistakes as done with traditional spam e-mails. AI has also been used to mimic voices using samples of specific individuals within executive positions.1 AI can also be used to create business documents such as invoices, contracts, spreadsheets, and bank statements.2 These documents can be created for valid purposes or to create fictitious transactions.

Fraud Cases involving AI Technology

AI technology has been used over the past several years to successfully carry out fraud. In 2019, deepfake technology was used against a United Kingdom (UK)-based energy firm to mimic an executive’s voice to mislead an employee to making a transfer of €220,000.3 AI deepfake voice technology was used again in January of 2020 to mimic a United Arab Emirates (UAE) Executive’s voice to steal from a subsidiary company, this time for $35 million.4 These cases highlight the dangerous capabilities of AI when used by sophisticated criminals. Firms must train employees on how to identify all scenarios and types of scams carried out with AI and how to react appropriately.

Use of AI to Prevent, Deter, or Detect Fraud

Whether fraud is committed with the use of AI or the use of conventional methods, the same technologies and capabilities that AI has created to perpetuate fraud are also used to uncover, detect, deter, or prevent fraud. Banking is an example of an industry that is currently effectively leveraging AI to prevent or detect fraud. Banks are using AI technology to detect suspicious activity via multiple capabilities, such as anomaly detection, behavioral analysis, and natural language processing.5 The measures banks are using with AI to detect and prevent fraud are a proactive measure of fighting fraud, which will prevent fraud before it occurs, as opposed to retroactively detecting fraud through a financial audit or forensic accounting procedures.

Safeguards to Consider for the use of AI in Fraud Detection, Data Analysis, or Other Uses

AI can and is being misused, and many important factors must be considered while either using or planning to use AI to analyze data. Organizations using AI technology must be cautious with the use of AI and form proper policies to adapt and consider security, quality and reliability risks, as results of data analytics using AI come from a machine and must be independently verified. A few important notes that financial and accounting firms must consider include the following:

- Learning as much about AI capabilities as possible to be able to identify AI-related fraud risks

- Verifying results produced by AI. AI generates information using a machine, lacking human judgment, and thus, results could be inaccurate, false, or susceptible to biases of the human(s) who developed the AI code

- Due to AI’s ability to create realistic business documents, whether for valid or fraudulent purposes, the need is greater than ever for accountants and auditors to continue reliance on third parties, such as banks to confirm bank balances and authenticate business documents

- For all types of businesses, to establish safeguards and policies for keeping internal company data off any Open-Source AI technology, such as ChatGPT. Also limit information (e.g., personal information such as travel, birthdates, addresses or other personally identifying information) posted on social media, as it can be used by AI to obtain information and carry out fraud.6

New Developments and Cases in the Use of AI

Figure 2: AI Beneficiaries

Corporations, such as Mastercard, and its competitor, Visa, are investing in Proprietary AI technology. Mastercard’s AI model will enable it to identify suspicious transactions in real time, and the company has invested billions in its AI technology.7 Other major corporations that are not primarily financial or banking firms are also heavily invested in and have implemented AI tools. For example, corporations, such as eBay and Zillow, are utilizing AI to help sellers and customers. eBay is using an AI tool to help sellers effectively write descriptions for item listings. Zillow is using AI in multiple ways, including using machine learning (ML) to identify high intent buyers and to help users easily search and find their dream homes.8

The Federal Government is also effectively leveraging AI to improve financial management, detect fraud, and increase accountability to taxpayers. The Department of the Treasury (Treasury) recovered over $375 million because of its implementation of an enhanced fraud detection process that utilizes AI at the beginning of Fiscal Year (FY) 2023.9 The important takeaways for these cases involving AI implementation are that most organizations, whether businesses, governments, or other entities, are finding innovative ways to apply AI to increase productivity, reduce fraud, and improve products and services for customers. It is vital for businesses and organizations to invest resources in AI initiatives to remain competitive.

Challenges of Implementing AI

The challenges of implementing AI will likely apply to smaller or less technology-savvy organizations, as well as organizations that may not have the personnel or financial resources to invest in and implement AI solutions and address risks surrounding its use. As business implement AI technologies, there will be reluctance due to the challenges listed in Figure 3. It is imperative that these challenges are addressed and overcome.

Figure 3: AI Challenges10

Key Considerations for AI as Applicable to Finance and Accounting Professions

Businesses that operate in the consulting, accounting, auditing, and regulatory industry must learn the capabilities of AI to understand fraud, security risks, and implementation challenges surrounding the use of AI, and in contrast, the benefits and ability to implement its use. As the use and investment in AI becomes common within the finance and accounting industry, it is essential to maintain a competitive edge in applying AI technologies, whether the technology is used in fraud prevention, data analysis, or to increase productivity. Specifically, AI technology will enable businesses to effectively support their clients through efficient data analysis, streamlined or automated processes, a better customer experience and cost savings. Information produced or output from AI is created by a machine and is susceptible to error. The output or results of AI-created analysis must be verified and validated before reporting for any purpose. AI technology is constantly improving but can still make mistakes if not properly vetted. Finally, consulting businesses will be in a position to provide services to establish AI Governance, which entails creating policies covering the acceptable use of AI, developing cybersecurity controls to manage information security risks that Open-Source AI presents, establishing requirements for compliance with laws and regulations regarding use of AI, and developing protocols for reporting findings and conclusions reached using AI technologies.

Connect with Us

This publication is for informational purposes only and does not constitute professional advice or services, or an endorsement of any kind.

Kearney is a Certified Public Accounting (CPA) firm focused on providing accounting and consulting services to the Federal Government. For more information about Kearney, please visit us at www.kearneyco.com or contact us at (703) 931-5600.

1How Is AI Used in Fraud Detection? | NVIDIA Blog | (nvidia.com)

2AI and fraud: What CPAs should know | (journalofaccountancy.com)

3A Voice Deepfake Was Used To Scam A CEO Out Of $243,000 (forbes.com) | (forbes.com)

4Fraudsters Cloned Company Director’s Voice In $35 Million Heist, Police Find | (forbes.com)

5Artificial Intelligence – How it’s used to detect financial fraud | (fraud.com)

6AI and fraud: What CPAs should know | (journalofaccountancy.com)

7Mastercard launches GPT-like AI model to help banks detect fraud | (cnbc.com)

8AI, Machine Learning & Research| (zillow.com)

9Treasury Announces Enhanced Fraud Detection Process Using AI Recovers $375M in Fiscal Year 2023 | (treasury.gov)

10What AI can do for auditors – Journal of Accountancy | (journalofaccountancy.com)